BIR Updates(October 12, 2020)

Deadline for availment of tax Amnesty on Delinquencies extended

BIR Updates(October 12, 2020)

Deadline for availment of tax Amnesty on Delinquencies extended

SSS Circular No. 2020-025

REVISED GUIDLINES ON THE MORATURUM ON SHORT-TERM LOAN PAYMENTS OF SSS MEMBERS AFFECTED BY THE CORONA VIRUS DISEASE 2019 (COVID-19) SITUATION

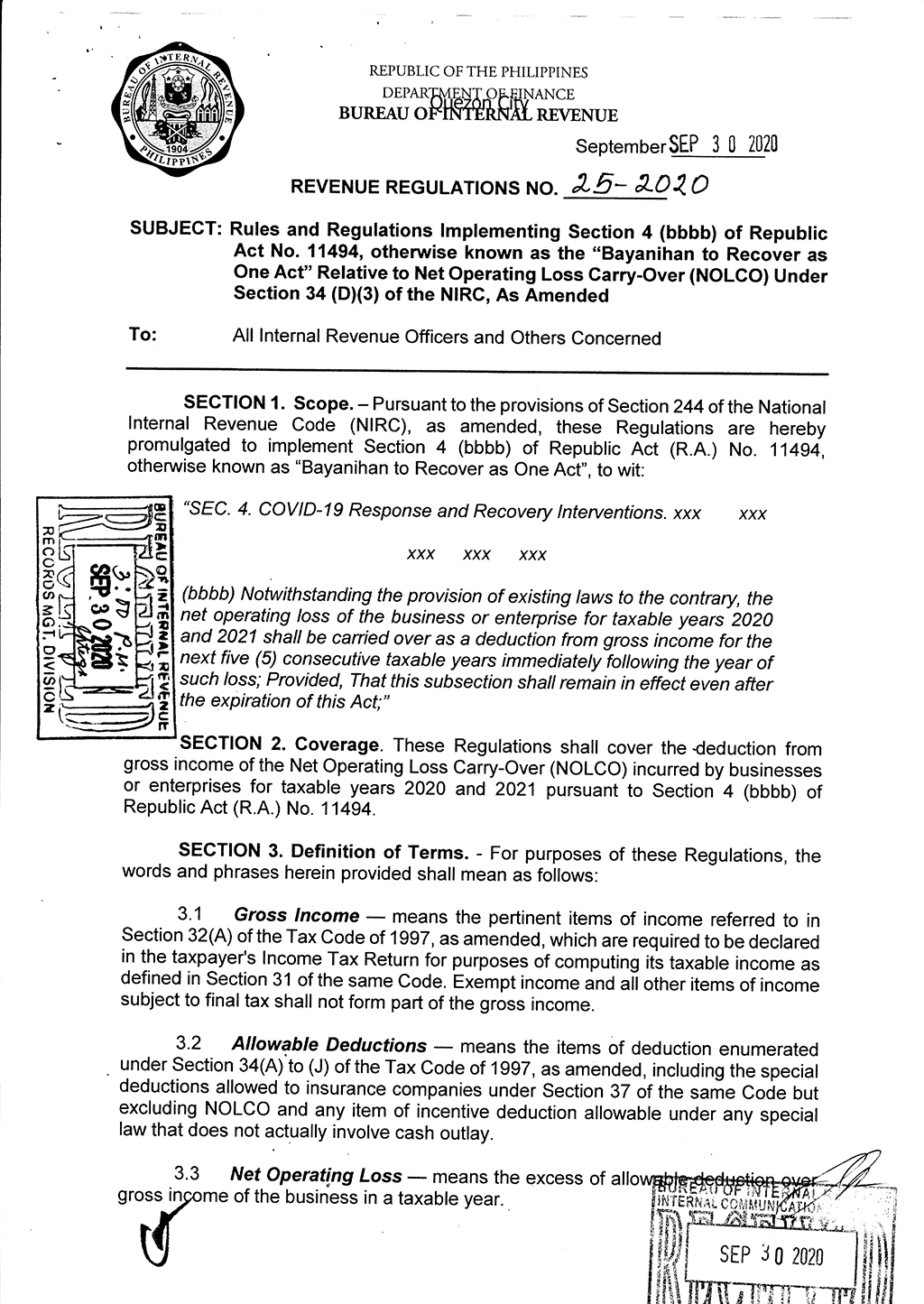

BIR Revenue Regulations No.25-2020

REVENUE REGULATIONS NO. 25-2020 issued on September 30, 2020 prescribes the Rules and Regulations to implement Section 4 (bbbb) of Republic Act (RA) No. 11494 (Bayanihan to Recover as One Act) relative to Net Operating Loss Carry-Over (NOLCO) under Section 34 (D)(3) of the National Internal Revenue Code (NIRC) of 1997, as amended.

Unless otherwise disqualified from claiming the deduction, the business or enterprise which incurred net operating loss for taxable years 2020 and 2021 shall be allowed to carry over the same as a deduction from its gross income for the next five (5) consecutive taxable years immediately following the year of such loss. The net operating loss for said taxable years may be carried over as a deduction even after the expiration of RA No. 11494 provided the same are claimed within the next five (5) consecutive taxable years immediately following the year of such loss.

The NOLCO shall be separately shown in the taxpayer’s Income Tax Return (also shown in the Reconciliation Section of the Tax Return) while the unused NOLCO shall be presented in the Notes to the Financial Statements showing, in detail, the taxable year in which the net operating loss was sustained or incurred, and any amount thereof claimed as NOLCO deduction within five (5) consecutive years immediately following the year of such loss. The NOLCO for taxable years 2020 and 2021 shall be presented in the Notes to the Financial Statements separately from the NOLCO for other taxable years. Failure to comply with this requirement will disqualify the taxpayer from claiming the NOLCO.

BIR Revenue Regulations No. 24-2020

REVENUE REGULATIONS NO. 24-2020 issued on September 30, 2020 implements Section 4 (uu) of Republic Act (RA) No. 11494 (Bayanihan to Recover as One Act) on the exemption from Documentary Stamp Tax (DST) of loans extended or credits restructured. The regulations shall cover all extensions of payments and/or maturity periods of all loans, including, but not limited to, salary, personal, housing, commercial and motor vehicle loans, amortizations, financial lease payments and premium payments, as well as credit card payments, falling due, or any part thereof, on or before December 31, 2020 contemplated under Section 4 (uu) of RA No. 11494, including the extension of maturity periods that may result from the grant of grace periods for these payments, whether or not such maturity period originally fall due on or before December 31, 2020. The regulations shall also cover credit restructuring, micro-lending, including those obtained from pawnshops, and extensions thereof made on or before December 31, 2020. No additional DST, including those imposed under Section 179, 195 and 198 of the NIRC, as amended, shall apply to term extensions and credit restructuring, micro-lending, including those obtained from pawnshops and extensions thereof granted by covered institutions for loans falling due, or any part thereof, on or before December 31, 2020. Interbank loans and bank borrowings shall be subject to the DST imposed under Section 179, 195 and 198 of the NIRC, as amended.

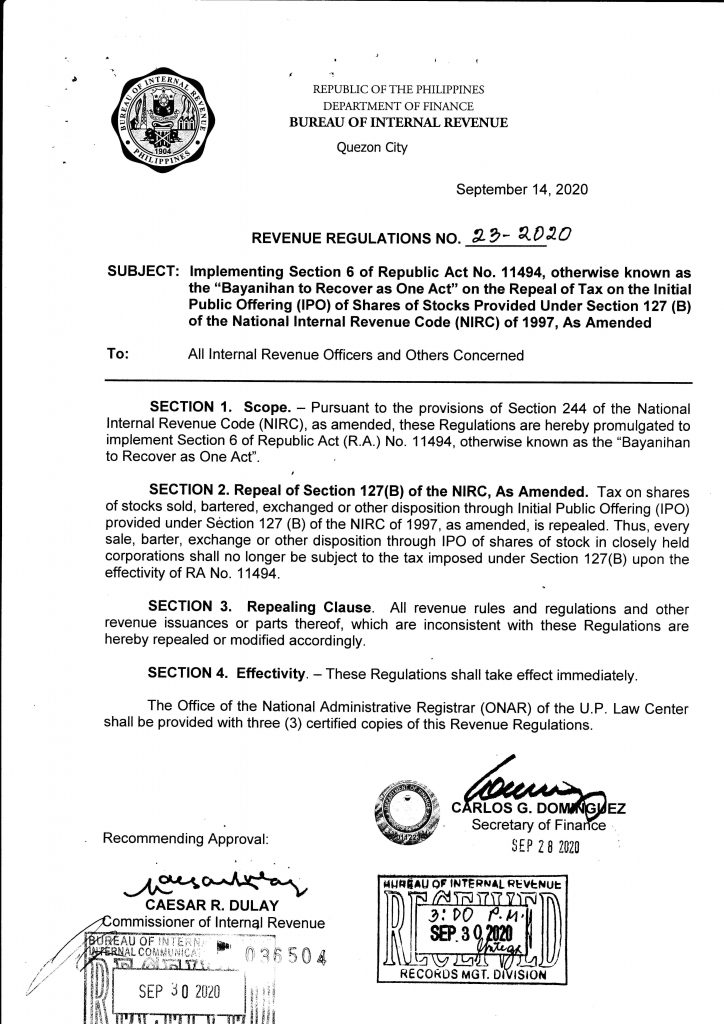

BIR Revenue Regulations No. 23-2020

REVENUE REGULATIONS NO. 23-2020 issued on September 30, 2020 implements Section 6 of Republic Act No. 11494 (Bayanihan to Recover as One Act) relative to the repeal of tax on the Initial Public Offering (IPO) of shares of stocks provided under Section 127(B) of the National Internal Revenue Code (NIRC) of 1997, as amended.

The tax on shares of stocks sold, bartered, exchanged or other disposition through IPO is repealed. Thus, every sale, barter, exchange or other disposition through IPO of shares of stock in closely held corporations shall no longer be subject to the tax imposed under Section 127(B) of the NIRC, as amended, upon the effectivity of RA No. 11494.