BSP Circular No. 1085 Series of 2020

Sustainable Finance Framework

BSP Circular No. 1085 Series of 2020

Sustainable Finance Framework

HDMF Advisory 27 March 2020

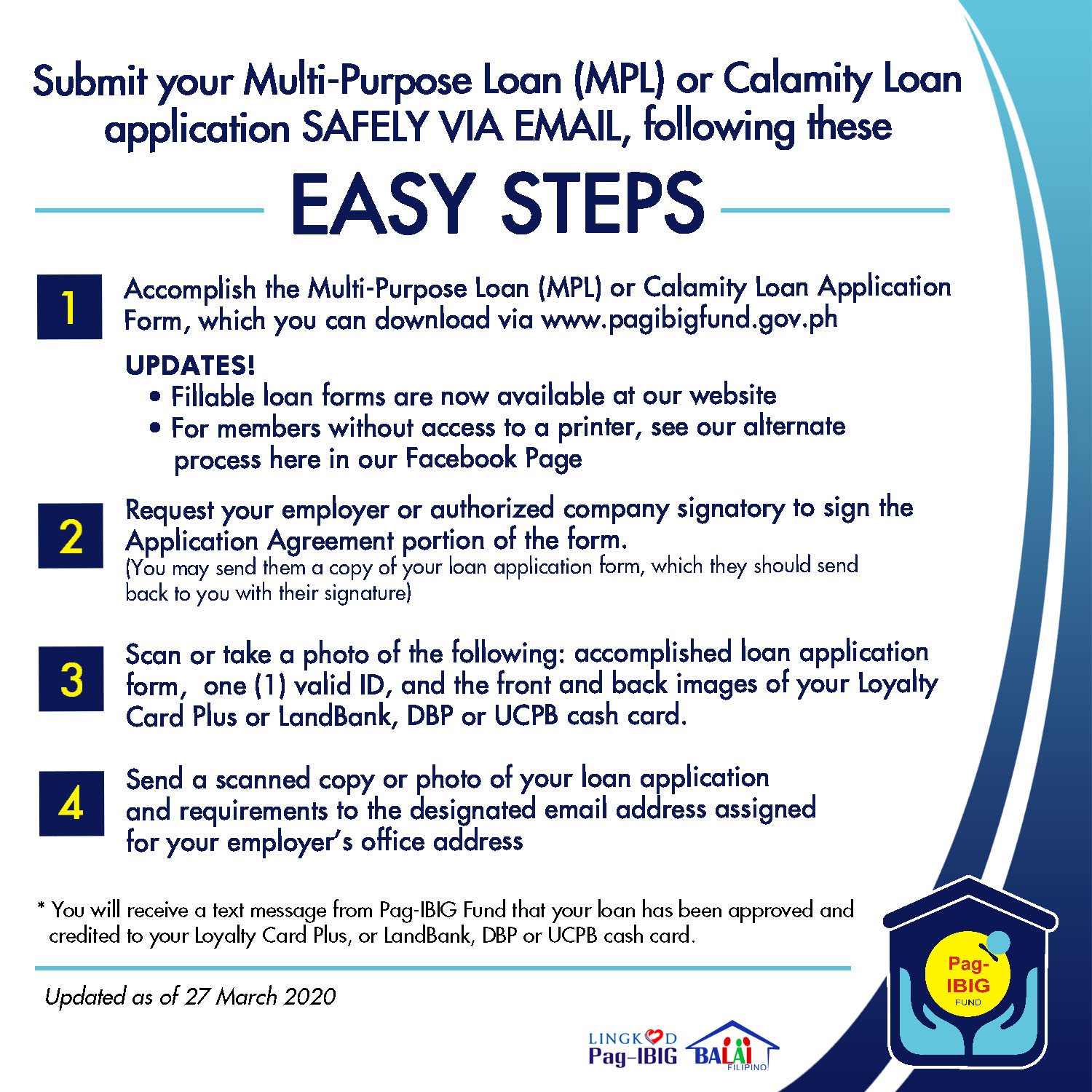

Online Submission of Multi-Purpose (MPL) or Calamity Loan application

PhilHealth Advisory No. 2020-27

Payment of Premium for all Direct Contributors

BIR Revenue Regulations No. 11-2020

REVENUE REGULATIONS NO. 11-2020 issued on April 30, 2020 amends Section 2 of Revenue Regulations (RR) No. 7-2020, as amended by Section 2 of RR No. 10-2020, relative to the extension of statutory deadlines for the submission and/or filing of documents and/or returns specified in the Regulations, as well as the payment of taxes pursuant to Section 4(z) of RA No. 11469 (Bayanihan to Heal as One Act).

The extension of due dates shall be made applicable throughout the Philippines. If the new extended due dates fall on a holiday or non-working day, then, the submission and/or filing contemplated in the Regulations shall be made on the next working day. Further, the term “quarantine” used in the Regulations shall mean any announcement by the National Government resulting to limited operations and mobility, including, but not limited to, community quarantine, enhanced community quarantine, modified community quarantine, and general community quarantine.

In case of another quarantine extension, the defined extended due dates under Section 2 of the Regulations shall be allowed further extension of fifteen (15) calendar days.

Taxpayers who will file their tax returns within the original deadline or prior to the extended deadline can amend their tax returns at any time on or before the extended due date. An amendment that will result in additional tax to be paid can still be paid without the imposition of corresponding penalties (surcharge, interest and compromise penalties) if the same shall be done not later than the extended deadline, as provided under existing rules and regulations.

A taxpayer whose amended returns will result in overpayment of taxes paid can opt to carry over the overpaid tax as credit against the tax due for the same tax type in the succeeding periods’ tax returns, aside from filing for claim for refund.

BIR Revenue Memorandum Circular No. 45-2020

REVENUE MEMORANDUM CIRCULAR NO. 45-2020 issued on April 30, 2020 circularizes Joint Memorandum Circular (JMC) No. 001-2020 (Guidelines for the Availment of the Small Business Wage Subsidy [SBWS] Measure).

The SBWS covers small business employers and their eligible employees, employed as of March 1, 2020, affected by the Enhanced Community Quarantine (ECQ) or other forms of quarantine imposed in Luzon and other parts of the country to address the COVID-19 public health emergency. A wage subsidy of Five Thousand Pesos (?5,000) to Eight Thousand Pesos (?8,000) (largely based on the regional minimum wage) shall be given to the eligible employees in two (2) tranches. Eligible employers for the SBWS Program are small business employers belonging to an industry classified as Non-essential or Quasi-essential in view of the Enhanced Community Quarantine and other forms thereof, imposed in Luzon and other parts of the country. Said employers must be registered in the BIR and have complied with their tax obligations in the past three years up to January 2020, and must also be registered in the Social Security System (SSS) and have paid SSS contributions in the past three years up to January 2020.

Eligible employees are those employed by an eligible small business employer as of March 1, 2020, and has been prevented from performing work for at least two weeks due to suspension of work, temporary closure, or the adoption of flexible work arrangement by his employer, in view of the ECQ and other forms thereof, imposed in Luzon and other parts of the country. The following employees are disqualified from availing of the SBWS:

a. Employees working from home or part of the skeleton force;

b. Employees on leave for the entire duration of the ECQ and other forms thereof, whether with or without pay; and

c. Employees who are recipients of SSS unemployment benefits and/or have unsettled or in-process SSS final claims.

Employees who have received benefits from the Department of Labor and Employment’s COVID-19 Adjustment Measures Program and other similar programs may be eligible under the SBWS, but the wage subsidy for the second tranche under the SBWS shall be net of any amount received from the said programs.

The employer, upon application with the SSS, shall certify that the employee has met all the eligibility requirements and none of the disqualifications.

Pre-qualified small business employers shall be notified by the BIR through the BIR website (www.bir.gov.ph). The pre-qualification conducted by the BIR shall not immediately entitle the small business employers and their employees to the SBWS. The pre-qualified small business employers shall still apply for the SBWS through the “My.SSS”, accessible in the SSS website (www.sss.gov.ph), unless notified otherwise by SSS through email. In which case, the pre-qualified small business employer shall apply by submitting the documentary requirements to sbwscertifications@sss.gov.ph. Applications shall be accepted by the SSS until May 8, 2020.

The small business employers shall include in their application the eligible employees based on the Eligibility Criteria for Employees specified above. Applications submitted manually or through other means not sanctioned shall not be entertained.

The SSS shall process and determine the eligibility of the employers and employees, in consultation with the Department of Finance (DOF) and the BIR.